What do the stock market and the game of musical chairs have in common? Will you be sitting comfortably when the music inevitably stops?

To my surprise, it's been over 5 years since my last post. Since then, much has changed, as we all know

I have read so many good quotes lately that I am not sure where the one above came from, but it certainly speaks volumes.

Twice a month, beginning in mid-February, I've been attending Zoom meetings with other financial planning colleagues from around the country.

“Pressure is what you feel when you are not prepared”

Lou Holtz

As I write this blog on Monday, February 24, 2020, the Dow is down about 900 points at mid-morning. Most analysts are pointing to the recent outbreak of the coronavirus in Italy and South Korea as spooking the markets, since this could set off a global economic slowdown. We shall see.

Have you ever said to yourself, when X happens, I’ll do Y? In other words, you’re waiting for the stars to align in your favor and then you’ll decide to do what you’ve been putting off for a long time?

In terms of financial planning, my sense is that too many people are waiting for the 'perfect' time to develop a comprehensive financial plan instead of moving forward when life, although not perfect, is pretty darn good. I would suggest that waiting for the perfect time is not only a risky decision to make, it could also end up costing you big time over the long run.

As many of my boomer clients get closer to that ‘magic’ number of enough savings to become financially independent, the concept of retirement, even just using the word ‘retirement’, is causing many to question what comes next.

Just last week, I came across a recent tweet written by Carl Richards. He’s the New York Times money sketch guy who writes a weekly column about behavioral finance.

The latest economic guessing game these days is predicting when the next recession will occur in the U.S.

Last week, I had the opportunity to attend a mid-year market outlook conference at Charles Schwab headquarters in San Francisco. There were four panelists; two from the equity side and two from the bond side of the investment world. Liz Ann Sonders, the Chief Investment Strategist for Schwab, was on the equity ‘team’. All four panelists agreed on two major themes; the global economy continues to slow down, and that a recession starting in early 2020 is a very likely possibility.

“Despite the good withdrawal rate, I still fear some catastrophic situation and imagine sitting on the curb as a bag lady! That, of course, requires a therapist--not a financial planner, eh?”

(This blogpost appeared four years ago, but it bears repeating.)

The above quote comes directly from a client, let’s call her Mary (not her real name) responding to an article I emailed her about the 4% withdrawal rule in retirement.

Imagine you just left your job/business/practice for the last time after an illustrious career of 42 years. Today was your last official day of working for money and tomorrow, as the saying goes, is the first day of the rest of your life.

A week has gone by since your last day of work. You’ve been super busy, you’re still waking up at 6:30 a.m., still following a tight to-do schedule, so the sense that you’re no longer working hasn’t really sunk in yet.

Imagine you’ve been following a customized financial plan diligently for the past 10+ years. I say 10+ years and not 20 or 30 years, because truth be told, in my experience as a financial planner specializing in retirement planning, most people don’t buckle down and take retirement planning seriously until they’re about 10 years away from this major milestone in life.

Now imagine the number, the number that’s been in your head, in your dreams, the number you’ve known about and thought about, the number that represents your financial independence, your financial freedom from ever having to work another day for money has been reached. Now what?

It’s the million dollar question and also one of the hardest questions to answer before you retire: When is enough, enough?

If you asked me that question back when I was a young and ambitious entrepreneur, striving yet never arriving, my answer most likely would have been never. You could never have 'enough'. Back then, I was a true believer that the sky’s the limit when it comes to earning money. More income meant more toys to buy, and anyway, how could one ever have enough?

You’ve made it to the ‘finish line’. You’re financially independent and retirement beckons. You’ve diligently saved for decades, and now retirement is no longer a fantasy - it’s as real as it gets.

Now, instead of adding to your savings, you enter the phase of your life where you begin withdrawing from your savings. You keep telling yourself you have enough money saved up to live the retirement lifestyle you imagined.

According to the AARP, 10,000 baby boomers are turning 65 every single day, and this is expected to continue into the 2030s. This means that nearly seven baby boomers are turning 65 every minute.”

If you’re a few years away from retirement, the day will soon come, when after a lifetime of squirreling away money and delaying gratification, the ‘distribution phase’ of your financial life will begin.

For years I’ve witnessed how we give too much of our power away when we visit our Doctor’s office. Instead of asking why they recommend we do x or y, we blithely follow whatever recommendation is made. After all, they’re the one with MD next to their name, so who are we to question their instructions?

With the political news, or should I call it the political storm-y brewing in DC, we might recall that it was only a few months ago that talk of a trade war with China and potential tariffs on steel and aluminum created dizzying volatility in the stock market.

It’s often one of the most common mistakes investors make. By that I mean, letting the amount of capital gains tax owed on the sale of your asset, whether that’s a stock, bond, real estate or business, dominate your decision process.

It’s never easy to pay taxes, especially a 20% capital gains tax. So instead of diversifying your overall investment portfolio and not concentrating too much of your net-worth in say one stock for example, you let it ride.

Soon, five, ten, twenty+ years goes by and now this asset that has strongly increased in value and makes up close to 50% of your total investment portfolio. You know having too many eggs in one basket is risky, you know and have seen and read enough about the importance of diversification and maintaining a well balanced portfolio, yet still, even with that self-awareness, you’re allowing the tax tail to wag the dog.

The dictionary would define 'legacy' as:

a gift or a bequest that is handed down, endowed or conveyed from one person to another. It is something descendible one comes into possession of that is transmitted, inherited or received from a predecessor.

A financial planner would define legacy simply as:

"the amount of inheritance you plan to leave to your heirs and or charities/organizations upon your passing.

Think about the last time you set a challenging goal for yourself. Maybe your goal was getting to a certain weight. Maybe it was acquiring a higher paying job. Whatever your goal was, there’s a good chance you set your goals at the start of a new year. So here we are again, with 2018 around the corner.

As you transition from work to retirement, you should be prepared for the inevitable emotional roller coaster ride you’re about to go on.

Year after year, client upon client all report that their first year of retirement, from an emotional point of view, is the most difficult year of all. What may surprise you is that the emotional challenges occur regardless of your net-worth.

Imagine, that after 40+ years of working and being accustomed to receiving a bi-weekly or monthly paycheck, suddenly, there are no more paychecks coming your way.

Of all the many challenges couples face in life, whether married or living together - deciding how as a couple you’re going to manage your money tends to be the most confounding.

Some couples choose to keep their money absolutely separate. This is mine, that’s yours, and never the twain shall meet, or something similar. Of course, this option which seems very straight forward, clear and easy, comes with its own set of problems not usually envisioned when initially making this choice. The main problem being, you’re not working as a team when it comes to coordinating your cash flow, investing and tax planning strategies. As a consequence, you’re missing the opportunity to optimize your finances. You would never run a business this way, so why would you manage your cash flow this way?

One of the main reasons people fail at retirement is they give too much money to their children.

Let’s say you’re in your 60’s when you retire or even early 70’s. At this time in your life, your children are adults, yet they’re still hitting up Mom & Dad for cash. What’s up with that? And how can or more likely, will that impact your financial security? Although every parent wants to see their children succeed, giving too much money away can cause a severe drain on a couples retirement resources and jeopardize their own financial security.

Let’s call this blog my annual financial planning public service announcement for those two years or less away from retirement.

At the end of the day, a financially successful retirement requires an honest assessment of where you are today, financially speaking. Although that sounds like a pretty obvious task to undertake, herein lies the problem.

I wrote this blogpost, Tax Planning Techniques & the Rise of the Backdoor Roth IRA a couple years back due to the intense interest from many clients about the Backdoor Roth IRA tax planning technique. It’s a bit surprising this savvy technique has not been shut down. It’s of course entirely legal and perhaps could be called a tax loophole. That said, as long as this option is available, why not take advantage of it? Tax planning at its core is about deferring taxes to a later date and or minimizing your current tax liabilities.

There are some big changes happening in the world of retirement planning. Some big and really good changes. First some background.

One of the most studied and researched topics in the field of financial planning is NOT the study of the accumulation phase of your life, where you’re saving and investing for the future. Instead, the subject that draws the most attention in the academic as well as professional world of personal finance, by a longshot, is that of the withdrawal phase of your life. The phase where you begin to distribute the money you’ve saved either with a planned retirement income strategy or a flying by the seat of your pants strategy.

The stock market has long been considered a leading economic indicator. Given the recent stock market rally since the election, it’s fair to believe 'the market' is sending a clear signal of what’s to come in 2017. Oh, but if only it was that easy.

One of the best money articles I read post-election in terms of what do I do now with my investment strategy was written by Ron Lieber of the Times in his Your Money column titled One Crucial Investing Question: Are Your Goals Different Now? Thankfully, this article makes you think long and hard before you decide to change your portfolio strategy.

Last week, a good friend asked me if I would look over the retirement plan his financial planner had just completed. Let’s call my friend, Steve.

And for the record, if I may digress, I’ve discovered the hard way that maintaining and keeping long-term friendships intact when your occupation is financial advisor, means making sure your friends understand why recommending they work with an independent advisor who is not their friend, yet puts their best interests first. Sounds easy, yes? Not so much. On to Steve’s story...

According to Pew Research, every day for the next 14 years, 10,000 baby boomers will reach age 65. Think about that for a second, that’s a lot of people. And whether they plan to retire at age 65 or in a few years, preparing for retirement is now front and center in their lives.

The way boomers define ‘retirement success’ is changing rapidly. The old model of ‘success’ - where your goal is to accumulate as much money as you possibly can by the time you reach the finish line, regardless of the stress and impact on your physical, emotional and spiritual health, well, that model is no longer sustainable.

This is a true story of a couple that planned on launching into retirement with high hopes, only to find their dreams dashed. It’s a story of betrayal, self-sabotage, unconditional love and the amazing gift of forgiveness and redemption.

There’s not many people in the financial world that have earned as much acclaim and adoration as the founder of Vanguard, John Bogle. Like his good friend Warren Buffett, these two men exemplify radical humility in an industry loaded with oversized egos.

On The Road to Retirement... “If you don’t know where you’re going, any road will take you there.”

The refrain "If you don't know where you're going, any road will take you there" was essentially a paraphrase of an exchange between Alice and the Cheshire Cat in Chapter 6 of Lewis Carroll's Alice in Wonderland: "Would you tell me, please, which way I ought to go from here?"

These past couple months, and especially the past few weeks, have been particularly nerve racking for investors. With memories of the last stock market crash still etched into our collective psyches, it’s challenging, even for disciplined long-term investors, not to get caught up in the frenzy.

Here we go again…..up, down, up, down. If this stock market roller coaster ride has you feeling anxious, you’re not alone.

It’s been a so-so year for investors in 2015. Lots of volatility throughout the year with little upside performance to show for it. I believe the title of this recent article says it best: The Year Nothing Worked: Stocks, Bonds, Cash Go Nowhere

With the recent enhancements high frequency traders have made, volatility looks to be the ‘new normal’.

In 2014, the Ibbotson/Morningstar asset allocation models we use when constructing portfolios projected an estimated return of 7.2% for a 60% allocation to equities and a 40% allocation to fixed income. At our firm, this would be considered a moderate risk portfolio.

Now, heading into 2016, Ibbotson is projecting a 5.27% return for that same 60/40 asset allocation. For investors with 10+ years before retirement, while not good news, it’s not the end of the world as you’ll have time to course correct if needed.

The stock market is volatile. Your bills are skyrocketing. Getting a grip on your finances, however, goes beyond your checkbook. Take a good hard look at your relationship with money, and you’ll finally figure out how the two of you can start getting along.

If your retirement is 10-years away or sooner, you'll want to read, Get What’s Yours - The Secret To Maxing Out Your Social Security by Laurence Kotlikoff, Philip Moeller and Paul Solomon

One of the most overlooked elements of preparing for a successful retirement is deciding when to start drawing your Social Security. If you’re a married couple, the decision becomes even more complex.

Up until recently, the majority of people, usually by default, either started collecting Social Security at their full retirement age, early, at age 62, or waiting if possible until age 70. Simple on the surface right, three relatively easy choices.

Guess what. There are dozens of Social Security strategies that most people are unaware of. And remember, in the game of money, strategy is king.

Next week, your monthly investment statements will arrive via mail or email. And unless your portfolio has been invested 100% in Treasury Bonds, you’re going to see unrealized losses on your statement, as it’s been a terrible month/quarter in the stock market.

It’s often impossible to explain stock market volatility until long after the dust has settled. And these past couple weeks of volatility are no different.

Since the stock market crash of 2008-2009, interest rates, especially the 10-year Treasury, have stayed historically low. Last quarter, the 10-year Treasury saw its largest rise since the end of 2013, halting a streak of five consecutive quarters of falling yields.

A couple weeks ago, a client in Oakland emailed me an article from Money Magazine titled: 4 Disastrous Retirement Mistakes and How to Avoid Them.

The premise of this must read article for anyone getting close to retirement and wanting to rollover their IRA is to see past the hype being touting by many a financial salesperson masquerading as an advisor, but really only concerned with their commission payout and not your financial wellness and security.

When was the last time you reevaluated your personal financial goals? Did you set initial goals when you were in your 20’s and haven’t looked back since?

If you’re a boomer, perhaps you’ll remember Hasbro’s famous “The Game of LIFE”? The Game of Life challenges players to manage their money and get to retirement wealthy. Different spaces on the game board offer life challenges like babies, houses, night school, you name it. Spin to win!

Should you include international stocks in your investment portfolio? If yes, how much? If no, why not?

When you think about financial independence (FI), what comes to mind? What do you imagine your life would look like if working for money was purely optional?

This is a question that many of my clients have pondered deeply and thoughtfully and continue to evaluate and review. Not needing to work for money and wondering what to do with your life once you’re FI is, as they say, a ‘gold plated’ problem we should all be fortunate enough to have.

But with so many possibilities, so many shades of financial independence to explore and discover, such a new dynamic and reality to accept and embrace - the choice of how you design your life plan truly matters. And it matters just as much whether you reach FI in your 40’s, 50’s, 60’s or 70’s.

Whether you earned, saved, lived within or below your means and invested well on the road to financial independence OR you received a windfall from real estate appreciation like many of my Bay Area clients are experiencing, especially those living in Berkeley or Silicon Valley OR you inherited your FI, the road ahead remains full of exciting possibilities. So which path do you choose? What now becomes your life purpose, your dharma?

And now, with the recent volatility, memories of those scary days still haunt many an investor that rightfully so, remains traumatized from that roller coaster ride from hell back in 2009. The thought that runs through many a mind in times of high volatility and high anxiety like we’re currently experiencing; is this going to be a repeat of 2009?

With so many books about money being published, how does one book set itself apart from another?

I just finished reading Flash Boys, A Wall Street Revolt, written by bestselling author Michael Lewis. The revelations in the book about how the stock market is being manipulated and rigged by high-frequency traders that have the advantage of speed, measured in milliseconds (a millisecond is a thousandth of a second) reads like one of your favorite mystery novels, only in this case, it’s not fiction but reality.

he·don·ism:

How much of a boost in net returns can financial advisors add to client portfolios? Well according to Vanguard, maybe as much as 3%.

To index or not to index - that is the question many investors ask themselves when building a durable investment strategy.

Imagine you’ve just met a person that not only has a black belt in karate, but a third degree black belt to boot and is a well respected and nationally acclaimed sensei (teacher). You’re in awe of the practice and discipline required to achieve this level of martial arts mastery.

Think about how many years of your adult life you spend accumulating enough money in order to have financial security and the lifestyle you desire when you stop working for money. You do your best, save as much as possible, live within or below your means, fund your retirement accounts, maintain a low cost, well diversified investment portfolio, and then the big day arrives, and you say adios to your job, career or business.

Suddenly, all those years of saving and accumulating come to a screeching halt and instead of being in the accumulation phase, you now move into the distribution phase with your money. On paper, theoretically, this all makes sense, right? Your nest egg now needs to last your entire lifetime. No worries, right?

I am pro-dream. There, I said it.

John Bogle, the founder of Vanguard, recently conducted an extensive interview with a financial insider publication called Money Management Executive. In this no holds barred interview, Bogle shares his opinions and wisdom on index funds, ETF’s and alternative investments and how they are being used and marketed to the public.

The following definition of ‘fiduciary’ is taken from the Center for Fiduciary Studies, fi360 website:

Like most financial advisors that have been in practice for over ten years, I have my fair share of clients that are millionaires. So with that said, what makes our millionaire clients different than your “average run of the mill” millionaire client? The answer; the majority are frugal and proud of it.

If you’ve read the best-seller, The Millionaire Next Door, you know many of the people portrayed in the book are, relatively speaking, pretty frugal. Keeping that thought in mind, and based on years of observation, below are the seven most common frugal habits of Spiritus millionaires.

In the hyper consumer society we live in today, buy now, pay later has become the norm. Saving enough money for a secure retirement all too often takes a back seat to the immediate gratification of purchasing the shiny object in the window. Practicing the concept of delayed gratification - fuhgeddaboudit.

If you’re like most people near or currently in retirement, you’ve spent most of your adult life managing your personal finances to the best of your ability. You’ve witnessed your share of stock market crashes, often referred to euphemistically as “market corrections”, you’ve saved and hopefully invested well, and you’ve done what’s needed to have a nest egg large enough to never have to worry about running out of money during retirement.

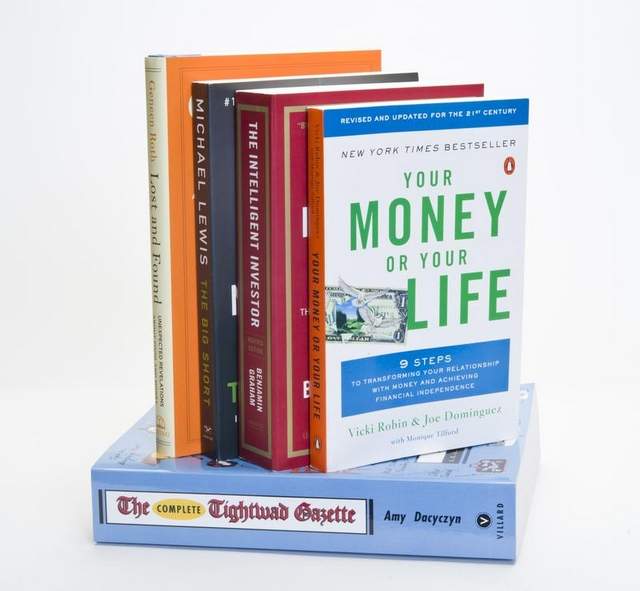

If you’re a fan of the New York Times bestselling book Your Money or Your Life - Transforming Your Relationship with Money and Achieving Financial Independence, it’s likely that 'achieving financial independence' (FI) part of the title that initially sparked your interest in deciding to read this seminal book on money.

But whatever the reason, as you find yourself dreaming and visualizing about financial independence you may also feel burdened and thrown off track by obstacles that are in the way of becoming FI. As you sit in yet another two hour commute to get to a job that drives you crazy, as you go through the third re-org in two years or get your fourth new direct report in two years or feel those crappy Sunday night blahs as you think about going to work Monday morning - as crazy as it sounds, these are all blessings in disguise.

If you’re among the millions of boomers beginning to plan for retirement, you’re most likely feeling a range of emotions that may range from euphoria to downright fear. Nonetheless, as you begin to prepare for this next phase of your life, step one is assessing where you stand financially right at this moment.

Yet on the road to assessing your financial readiness for retirement, unexpected events could occur that rock your world and change your life in ways probably unimaginable to most people. The story below actually happened. Names have been changed but events that occurred are unfortunately real.

This description is taken from Wikipedia:

If you’re the type of person that’s a planner by nature, then most likely you’re also good at establishing financial goals grounded in reality, goals that are achievable, and that also require a bit of a stretch. After all, if you’re goal oriented, setting goals that are too easy to reach can’t compare to the thrill of reaching or exceeding a personally challenging goal.

When Pat and I are away for the weekend, we don't stay digitally connected. Part of the whole reason for getting away is to unplug from our daily lives. Even though we both own smartphones, we don't keep them turned on unless we are looking for a restaurant recommendation, need directions or meeting friends.

This past weekend we headed off for Mendocino. Since we were going to connect with a friend while there, I turned my cell phone on and checked my email only to discover a fraud alert notification from Chase. The email was alerting me about a suspicious attempt to use my credit card earlier that morning. Since the transaction was coded as suspicious until cardholder verification, the transaction was denied. Pat and I checked to see if we both had our cards, (we did), but the attempt was made using a physical card.

"Permission to be a beginner again is the greatest gift you can give yourself."

The following is an excerpt from a recent article, titled, For Retirees, a Million Dollar Illusion, that appeared in the New York Times, Your Money section. Anytime there’s an article that discusses your ‘number’ needed for a safe and secure retirement, I’m hooked.

The article drew so much attention and received so many follow-up comments that the author actually wrote a follow-up to his original article. I encourage you to read the original article in full as well as the follow-up and see for yourself if $1 million is enough to safely retire.

If you are looking to diversify your investment portfolio, (and you should be) here are two alternative investment strategies worth considering. But first, full disclosure: We have absolutely no affiliation to the firms mentioned below and receive zero compensation or any compensation, financial or non-financial from these firms. At times, we will recommend and acquire these investments to add to our investment management clients’ portfolios. Both investments come with risk of loss, so you need to do your due diligence before investing.

Peer-to-peer lending has been popular in Europe for many years and it’s finally getting its due attention here in the states. The two leading companies in this space are Prosper and Lending Club.

By creating a virtual platform bringing together borrowers and lenders aka-peer to peer- outside the conventional banking system, peer to peer lending is surely going to become more and more popular as word spreads. NPR recently did a story on this new concept that you can read or listen to.

I had the pleasure of meeting one of the owners of Prosper at a recent breakfast meeting in San Francisco. His vision, strategy and track record left little doubt in my mind that this is an alternative investment that needs to be seriously considered.

Prosper for example offers 1, 3 and 5 year notes for investors with varying interest rate returns depending on the borrower’s credit score and overall risk profile. Monthly interest payments can be reinvested or deposited electronically into your checking account.

Lower risk seasoned returns at Prosper currently average 5.41% with higher risk notes earning 14.12% and higher. Investments in personal loans from qualified borrowers can be as little as $25. For fixed income investors seeking higher income, this could play a role in your portfolio. Being able to invest across different credit grades and estimated yields provides the diversity you need.

Perhaps it was my 3 years of experience working at Fair Isaac, home of the FICO credit score, that has me believing in this alternative investment so highly, yet peer-to-peer lending/investing in my humble opinion is the next big thing in the investing world. Check it out, make sure you fully understand the risks involved and see if it has a place in your portfolio.

“A person saving for retirement who chooses low-cost investments instead of higher-cost ones could have a standard of living throughout retirement that's more than 20 percent higher”, says Noble Prize winner William Sharpe.

In a recent interview published on the Stanford Graduate School of Business website, Sharpe, a professor emeritus at the school, clearly illustrates how much more money retirees would have if they saved for retirement using lower-cost index funds rather than higher-cost actively managed funds.

A couple of weeks back, I received a call from a client couple, (who I’ll call ‘Z’) who have been happily retired for a few years. During our conversation, they let me know they needed to take out some extra money for a one-time expense that their regular retirement income won’t quite cover. However, this isn’t the first time; in fact, it seems for client couple Z there’s a different one-time request more years than not.

I've noticed that there is a sense of urgency as you get older, time speeds up, the questions of a good life lived haunt and nag. For some, that 'as you get older' point is approaching 60, for others it's turning 30, but at whatever the age the questions start, you might want to give them some attention.

Adam Shepard was a 30 year old with more than a mild case of wanderlust - he wanted to fully live every single moment, not to miss a single opportunity presented to him, to really experience life in every way possible. So he sold everything, took off for a year and then wrote a book about his experiences called 'One Year Lived'. But before he did any of that - he carefully developed a plan on how to accomplish his dream. Adam is not a Spiritus client, but someone who sets goals and achieves them, he’s a follower of his dreams, a thoughtful and careful life-planner, a risk-taker and an incredibly enthusiastic and over all friendly guy. And his book is not just interesting in terms of experiencing other cultures and countries through his eyes, but he’s crazy funny in his descriptions and in the situations he gets himself into.

Here in the wealthy enclave of the San Francisco Bay Area, it seems and feels like ground zero for the everlasting internal debate between quality of life vs. standard of living.

The Roth IRA has been one of the best tax planning techniques to come out of Washington, DC in a very long time. But because the Roth comes with income limit eligibility limitations; (maximum income for singles in *2017 - $133,000 ) and (maximum income for married couples - $196,000 ), lots of high income earners have been unable to take advantage of this option. *These dates and figures have been updated for 2017.

Like many of you, including yours truly, that have already received loads of info about the ‘backdoor Roth IRA’ from tax planning firms or your CPA, below is a consolidation of the best of the best that I have received recently on this topic. All due credit belongs to the numerous sources that kindly sent me info about the new ‘tax kid’ on the block - the backdoor Roth IRA - thank you!

We are currently in the midst of one of the largest transfers of wealth from one generation to the next that our country has ever witnessed. That’s because as parents of baby boomers start to pass, the legacies they are leaving behind in the form of inheritances are in the trillions of dollars.

Last year alone in our financial planning practice, one out of three new clients contacted our practice as a result of receiving an inheritance. And in many cases, the inheritance they received was a game changer - meaning the amount received was large enough to create financial independence.

Mistakes, lies, omissions, inflating the truth - these can all amount to the same end. Major problems with the IRS and a possible audit.

This is a guest post from one of my dear clients Stacie, who I wrote about in an earlier blogpost about her budding journey toward living her own dream.

Giving your power away when it comes to your money is an age old affliction that affects both men and women, the rich as well as the poor, the famous and the non-famous, the young as well as the old.

If you’re a single boomer and find yourself happily or begrudgingly back in the dating scene, it’s only a matter of time before the right person comes along and captures your heart as well as your imagination.

For the next 19 years, close to 10,000 boomers will turn 65 everyday and the majority will also be heading into retirement.

Back in the day, I considered myself an ‘outsmarter’. It was the mid-80’s, I was young and carefree and believed, as did the vast majority of my friends and colleagues, that we had the winning formula for stock market success.

Today I had a Skype call with one of my favorite clients. Stacie, a 1st generation American, is in her late 30’s, currently lives in Florida, and up until very recently, had a very successful and lucrative career as an engineer for a global consulting firm. Stacie had the type of career that her family had dreamed of for her, and her parents were willing to immigrate to the U.S. to ensure that she could have.

If you’re like the majority of people, come the New Year, you feel almost a primal urge to do something about your finances.

It may be something simple like checking to see how your investments performed last year or perhaps something more ambitious like developing a comprehensive financial plan.

What exactly you do is not the point, but definitely do something, anything, just get started. What you’re looking to do is get into the habit, at least once a year, of investing some time in not only how your relationship with money is going individually as well as with your partner, but also in assessing the previous year from a your money and your life holistic perspective. Call it the year in review.

Facing reality when it comes to planning for a successful retirement is easier said than done. For many people, just effectively managing their day to day finances is already a daunting challenge. Add to that list of to-do’s developing a realistic retirement plan and you risk becoming overwhelmed by it all.

What often happens instead is a form of denial and fantasy. We tell ourselves that somehow, someway, our investments will reap double digit returns from now until retirement day. That our incomes will double and cash windfalls are right around the corner. That the 20,000 shares of that penny bio-tech stock we purchased will be worth a million or more dollars in ten years and our home will be worth much, much more than we ever anticipated down the road.

Some of the world’s leading economist’s have discovered something that is especially relevant as we get ready for Thanksgiving.

As the holidays approach and your credit cards get ready for their annual workout, please, make a promise to yourself that before the end of this month you’ll take action and place a credit freeze on your credit reports for all three major credit bureaus.

If you’re a baby boomer, you most likely grew up with the notion that men are born with a natural ability to be good at managing money and investing.

When it comes to professional investment or financial planning advice, clients want to work with someone who is both competent and committed to serving their best interests, someone that honors and values integrity as a core belief. In short, they want someone they can trust. They want a fiduciary.

Maybe you’ve just received an inheritance, or you’ve decided to get your financial house in order by developing a comprehensive financial plan, or you’re preparing for retirement and you’re seeking the guidance of financial planner. Whatever the reason for contacting me, I often get asked the same questions:

I'll warn you up front, the article The Inadequacy Of Our National Savings, appearing in the current issue of Financial Advisers magazine is a long one, but information you really can't ignore.

When was the last time you talked, and I mean really opened up and spent some quality time, with your significant other about your dreams and aspirations for the eventual next phase of your life - retirement or early semi-retirement?

Who could have guessed back in January that Vanguard stock mutual funds would have performed as well as they have year to date?

Based on a recent trip back east to visit my elderly parents and in-laws, I realized that for some, stressing over money never ends. Even though I have reviewed both sets of parent’s financials and showed them they are in fine shape, they still worry that they won’t have enough to last their lifetimes. The one difference is that for both of them, their first priority is making certain the kids get an inheritance. In our case, our parents have plenty of money to see them through the end of their lives, and the inheritances they planned on giving are a reserve to dip into should they need it. I imagine it is part of that generation in having a legacy of giving – so unlike the bumper stickers I often see affixed to RV’s stating “I’m spending my kids inheritances.”

I wrote a blogpost a few months back titled 'Make Financial Integrity #1 When Choosing an Investment Advisor, where I attempted to clearly define the lay of the land in regards to the financial industry - specifically the investment advisor role. Today I came across a similar article written so well, I have to share it with you.

Rueters columnist Mark Miller, in his article 'Shakeup Complicates Finding a Good Financial Adviser, expresses how as a result of recent difficult financial markets and tougher regulations, it is becoming more challenging to find a financial adviser to match you and your needs. He navigates the reader through the process by explaining the differences between financial advisers from brokerage firms and (often independent) fee-only planners. He goes on to describes what an RIA is and what their responsibilities to their clients are. He discusses the future of financial advisers and explains what is going on in the industry. He talks about fraud and enforcement of rules and regulations and then ends his article with a few solid takeaways.

Back in the day, I was a spender - a big time spender actually. It was the late 1980’s, the economy was starting to really take off and President Reagan had just lowered taxes across the board. I was in my late 20’s, earning a six figure income as a partner of a fast growing financial consulting firm. Life was good.

If you find yourself just about ready to say yes and commit to the development of a comprehensive financial plan but for some reason you keep getting stuck on making the final move, my guess is the thought of compiling the documents needed is your roadblock.

So imagine my joyful surprise when a new client just emailed me her very positive feedback after gathering all the info needed to design her financial plan...

During their working years, baby boomers have invested a significant portion of their retirement savings in stocks, boosting equity valuations above historical averages for the past 30 years. As the baby boom generation retires and begins spending from their investment portfolios, future equity returns could decrease. With that in mind, it’s crucial that boomers nearing retirement develop retirement income strategies with prudent as well as realistic expectations of future investment returns.

The Role Demographics Will Play

Yet another study - this one telling me something I've noticed in my own financial planning practice for several years. According to Prudential Financial's latest study, The Financial Experience and Behaviors Among Women, 53% of the 1,400+ women surveyed are primary breadwinners in their households. The study polled 1,410 American women and 604 American men between the ages of 25 and 68.

Women are taking on the primary breadwinner role for several reasons; because of their partners loss of employment as a result of the financial crisis, as a result of divorce and because women are marrying later in life.

Investing, managing, saving, spending and earning money - these linear, left brain aspects of our money relationship offer plenty of potential for challenges. But it’s when we delve into the other dimension of our relationship with money, our feelings, that things get really tricky and mighty interesting.

Our feelings, that messy and confusing aspect of our relationship with money will often hold us hostage to our egos and prevent us from feeling the fulfillment and peace of mind we so desire. Way too many of us live our lives with feelings of scarcity and poverty consciousness. Instead of money being our servant, it becomes our master.

And now for the bonus round - a few multiple choice questions about Americans and retirement.

Thanks to my friend and client Eddie Mac for passing on this excellent article about raising your kids with a good set of values around money.

Of the many aspects involved when designing a comprehensive financial plan, probably my favorite element of all is helping clients decide on their number. The number I’m referring to is your total net-worth, but more specifically, the amount of liquid assets you’ll need to accumulate by the time you’re ready to retire or stop working for money.

Imagine for a second you and your life mate are headed out on a 30+ year journey, one that you had been planning to take for as long as you both can remember. You’ve dreamed about all the places you’re going to visit and the people and friends you’re going to meet along the way.

You know given your age, this will likely be the last, yet greatest adventure of your life with memories and experiences you’ll cherish forever. And vital to the success of this journey will be the confidence and knowing that the hard earned money you saved your entire working life will last the duration of your great adventure called retirement. You also know that once you set sail for the great unknown, there will be no chance for a do-over 10-15 years from now if you failed to properly plan.

There’s really no easy way to define the experience of waking up your first Monday morning after a lifetime of work, and realizing you’re retired and financially independent. You made it! You don’t have to go to your cube/office/practice/business again - EVER.

For some, this first Monday morning is a Zen experience, transformational in essence, very spiritual and very powerful. For others, it’s one of the most terrifying days of their life.

When was the last time you dreamed about the life you imagine yourself living, the career or business you see yourself owning, the soul mate you see yourself marrying and loving, the abundance you see yourself manifesting?

Although not news to me – you might find it shocking and certainly disturbing to discover that some financial advisors will sometimes work against their clients best interests if – guess what? If the advisor can pocket more money in fees.

According to a new study, done by Cambridge Mass. based National Bureau of Economic Research, (NBER) many advisors will encourage chasing high returns and press clients toward funds with higher fees. This was discovered after NBER sent out auditors, posing as clients, to almost 300 financial advisors in the Boston area.

What will it be for you? Ahhhhhhh retirement.... or AHHHHHHHH retirement!!!

You may be one of the lucky (but very few) who have no retirement worries as a result of a generous and secure pension. For the rest of us, there is some very careful and strategic planning to be done. But before crunching the numbers, it’s imperative to begin with the emotional side of retirement planning.

One of my clients recently let me know that she and her husband were taking their kids on another international trip - this time to enroll them in college. I sent her the link to Maya Frost's blog about studying abroad. Maya's book The New Global Student, will give you creative ways to cut college costs while at the same time scratching your wanderlust itch.

The following article written by Maya Frost, appeared in the Spiritus newsletter in Jan 2010.

It's true - if you want to achieve financial success, you'll need to develop your delayed gratification skills.

I never believed that a parent can’t have a favorite child – then again, I’m not a parent. But as a financial planner, I will admit that I do have favorite clients – my ‘Your Money or Your Life’ clients. We speak the same language; we understand the idea of having a healthy relationship with money, we get the concept of money equaling life energy and we value, value. We are inherently frugal and we are huge advocates of setting goals, such as becoming FI.

With the re-issue of the book in 2008, I have seen an influx of clients either having read the book for the first time, or re-aquainting themselves with the philosophy and for that I am grateful to Vicki Robin for the opportunity to have contributed to the latest edition.

Sunset magazine had an article in the Feb 2012 issue featuring 20 'dream towns' in a best places to live list. The criteria was that these towns had to be slow paced and stress free - not easy to find anymore in our crazy busy world.

Who could resist fantasizing about taking off for Nelson, BC or Whitsunday Islands in Australia. It's interesting to read about these couples who actually did it, leaving behind friends, family, careers and homes in search of a more mellow lifestyle.

When it comes to retirement income planning, one of the most important decisions you’ll make is the assumption for your projected rate of return.

Before the market crash of 2008, counting on your retirement savings growing 8, 9 or even 12 percent plus, year after year after year, are likely gone. In the ‘new normal’, cautious investors are learning to revise their expectations downward and for good reason. Recent market volatility, the debt crisis in Europe, a slower growing global economy, a weak real estate market and political gridlock have all contributed to revisiting long-term growth forecasts.

You Are Not Your Net-Worth

For any person on the journey to financial independence (FI), one of the most daunting tasks to contemplate, as well as figure out, is how much is enough?

How Much is Enough & The Nature of Fulfillment

You know the importance of having a will and power of attorney, but have you considered the peace of mind a letter of instruction would provide to your family once you are deceased? Along with developing a financial plan, preparing a letter of instruction is a responsible step to take in your family's comfort and security.

Simply, a letter of instruction is an informal document that provides your loved ones basic instructions and information regarding your assets and debts. We spend a lifetime caring for and loving our family, and taking this last planning step in preparing a letter of instruction will help make the transition smooth and less stressful for them. I want to be clear - a letter of instruction does not take the place of a will, but is used along with that and the other important documents such as a durable power of attorney, etc.

You don't want your loved ones to be trying to find any of this important information in their time of grief. You'll want to spell out very specifically where they can locate the following:

As a fee-only financial planner, I receive weekly industry publications which for years now, have been coaching us ‘financial types’ on how to really talk and connect with our clients. These publications continue to warn us that the ‘trend’ is going toward a more personable client/financial planner relationship. It worries me to think that someone has to be trained to care about the people they are working with. Like doctors, we are not all cold and numbers obsessed, many of us have a great bedside manner – and for some, it comes naturally.

Helping people understand personal finance and then make good financial decisions is what keeps me in business.

In a recent survey by Fidelity Investments, 500 couples were asked about their plans for retirement. The survey targeted couples near retirement or those who had already retired.

What the survey revealed was that although many couples work hard in the savings aspect of retirement – they do a very poor job at communicating with each other about their individual goals, dreams and expectations around retirement. Since they hadn’t previously discussed it, a large percent of couples reach retirement age without having decided on the big questions like where to live or at what age to retire.

The following is a guest post by my friend and colleague, Diane Williams who along with her husband became FI (financially independent) after reading the book Your Money or Your Life. Their story is both inspiring and exciting and I would encourage anyone who wants to know more about how they achieved FI at age 50 to contact Diane.

The public has received a hard earned education when it comes to finance and investing. The upside to the Bernie Madoff’s of the world is that consumers are now becoming savvy and more informed about how they manage their hard earned money – and who they trust when investing it. I'd like to offer a little more education when it comes to choosing an investment advisor.

For years, great thinkers and spiritual leaders, past and present, have written about money and spirituality. Often illustrated are step-by-step instructions on how to tap into and access your spiritual power to manifest abundance into your life.

Books such as Think and Grow Rich by Napoleon Hill, The Seven Spiritual Laws of Success by Deepak Chopra, The Power of Intention by Wayne Dyer and Living in the Light by Shakti Gawain are just a few examples that open your mind to a new way of manifesting abundance into your life.

Since the stock market crash of 2008, investors of all stripes, but especially boomers, have had a love-hate relationship with the market. When the markets are relatively calm and trending up, we love the markets, when the opposite is true, we hate the stock market.

I’m purposely using words like love and hate to illustrate a point. These are powerful words that in turn create powerful and impactful emotional responses. And if there’s one area of life that truly benefits from rational decision making as opposed to emotionally based decision making, it’s the world of investing.

We’re only three weeks into the New Year and hands down, almost every potential client I’ve spoken with so far is concerned about one thing and one thing only - retirement planning. More specifically, they want to know, based on their current financial picture, if they’ll be able to maintain the lifestyle they desire when no longer working for money. That, ladies and gentlemen, pardon the cliché, is the $6 million dollar question on many a boomers mind these days.

Where most of us do really well is on understanding and executing on the accumulation phase, such as saving and investing X amount in your IRAs, 401ks, 403bs, each year. We get that concept. Where things become murky for many people is when you get to the income distribution phase of retirement planning. This is when you need a long-term strategy to fill the gap between your social security and possible pension payments and your lifestyle expenses. To do that, you ask the following questions:

According to the Transamerica Center for Retirement Studies, a measly 8% of employed women feel they are building a sufficient retirement fund. One of the main reasons for this is that women aren't talking about retirement planning.

So to remedy the problem, and based on it's research, the Center for Retirement Studies came up with some questions that family, friends and advisors can ask women to get them started with talking about retirement.

Can you guess the average age at which we are at our mental sweet spot?

How much money does it really take before we consider ourselves to be rich? Based on net worth and income, this infographic by Mint.com, which is based on a recent Gallup poll reveals just what we Americans believe the 'rich index' is.

This is the time of year people often start thinking about getting their financial house in order. So if creating a personal financial plan is on your list as a personal and financial goal to accomplish in 2012, you won’t be alone. As you survey the landscape of fee-only financial planning options available, keep this in mind;

Creating and implementing a comprehensive financial plan that

Yesterday, a slew of articles appeared in the news proclaiming Married Couples at a Record Low. I’m aware of the trend that younger people are delaying or reevaluating whether they want to make the plunge, and with over 50% of marriages still ending in divorce, I can understand the hesitancy.

So as we prepare to bid farewell to 2011 and ring in 2012, I find myself wondering, will money continue to be one of the major causes of couple’s calling it quits?

Although poor investment choices and shoddy money management habits pose some of the greatest risks to your long term financial security, an additional risk that’s not often considered is the risk our over demanding egos pose to our financial freedom.

It's the ego that wants us to believe that we are how much money we make, the job title we hold, the type of clothes we wear, the home we live in or the car we drive. It’s the ego that demands we compare ourselves to our colleagues, neighbors, family members and even celebrities. The ego has us continually striving yet never quite arriving. And most toxic of all, it’s the ego that convinces us our self-worth is linked indelibly to our net-worth.

Are you planning on a miracle or planning for success in 2012?

I heard two new great phrases pertaining to money this week. The first was “living below your means” which I wrote about in a previous blogpost after hearing Suze Orman promoting her new Money Class. Living within ones means is now a common phrase, but below ones means? – now that’s a concept that I truly hope goes viral.

The second phrase appeared in an article one of my favorite clients, Eddie M sent me – the phrase is “time affluent.”

Of all the many golden rules when it comes to managing money, one of the most classic and familiar is to “live within your means”. How many times have you heard that expression?

But how about “living below your means”? Suze Orman, (whose style is not my favorite, but whose message is clear and spot on) has a new series called The Money Class which is where I heard the phrase living below your means. I’ve watched some of her specials before, yet I think this is her best yet. From the intro I watched on PBS, I believe this Money Class series is going to really benefit many, many people in bad financial shape.

No, this is not an oxymoron. Over 200 people that make over one million dollars per year are asking, practically begging, the leaders in Washington to raise their taxes. I have never seen anything like this in my life.

To counter the image that most if not all wealthy people are greedy and only care about their own self interest, this group of citizens are determined to shake things up and let us all know that they deeply care about the social contract we have with all our fellow citizens and that they are deeply passionate about our collective common good.

I'm a big a fan of former U.S. Secretary of Labor Robert Reich, so I wish I could have been on the steps of Sproul Hall at UC Berkeley last night where Reich gave the annual Mario Savio Memorial Lecture.

Reich called his speech "Class Warfare in America," and he talked about the concentration of wealth in the US at the top of the economic pyramid, and what he called, "the irresponsible use of wealth to undermine our democratic system.”

Last week Lemony Snicket's Daniel Handler wrote these 13 Observations on Occupy Wall Street. I caught him on Rachel Maddow's show last Friday where he shared the story of how these observations came about.

While taking a swim at his health club, he found he had to share a lane as it was a little more crowded than usual. The guy he was to share the swimming lane with wasn't too happy about it, and had no intentions of sharing his lane because, "I'm a major donor in this building, so I don't think I have to share a lane."

When considering the retirement alternatives out there - people are getting more and more creative in their thinking. Karen DeMasters outlines some other options you may not have considered, including what is known as a '"transitional strategy', in an article she wrote that appeared in the most recent Financial Advisor magazine.

In laying out a case where when approaching retirement, one has to balance both time and money, the article states, "T. Rowe Price believes that even if you both work part-time in your 60's while you begin playing, the financial benefits may be significant, or, in some cases a couple may choose to have one spouse retire while the other continues working." It's not often you read an article about retiring with the phrase 'funding your fun' in it.

Over the years, I’ve heard the same concerns again and again by people who are dipping their toes into the financial planning waters for the first time. As when I started Spiritus Financial nine years ago, my aim continues to be on financial education and empowerment, not on selling. The more you learn about money – the more successful you’ll be financially. So here they are, the five most common myths I’ve encountered in my financial planning practice.

I suppose that depends on how one defines risk. I define it as running out of money before you run out of life. If a major allocation to fixed income will produce returns that virtually assure you of depleting your portfolio in this lifetime, how can one define that as a low-risk portfolio?

Adding the appropriate allocation to equities may create more fluctuation, but it could reduce the risk of running out of money. Before constructing an investment portfolio, one must not only measure 'risk tolerance,' but the return necessary to achieve their goals.

In an recent article by the Financial Planning Association (FPA) a 2010 study of wealthy female investors showed that women were more likely to consult a professional advisor than men. One reason is that women in general are more cautious or conservative when making financial decisions.

According to the study, in addition to seeking professional financial advice, women are opting for more education around money issues. And just like the old stereotype about the differences between men and women in asking driving directions (in pre-GPS days) - women are not afraid to ask for financial guidance and advice.

I'm not saying it's fair, not by a long shot, but these are some facts about women in the workforce:

Women who take charge, do the math, plan for contingencies and work with their partners and/or financial planners have a better chance of securing their finances in retirement than those who shrink from the process, according to a new study.

The MetLife Study of Women, Retirement, and the Extra-Long Life: Implications for Planning, shows women face a number of unique financial risks—including outliving retirement funds, aging single, lower retirement incomes, greater health care costs and added care-giving responsibilities—and have not planned adequately to address these concerns.

Slightly more than half of the women surveyed know the likely amount of their retirement income/assets and only 44% have calculated the amount of their essential expenses, according to the study. Approximately one-in-six (16%) reported that they have or plan to delay retirement, on average, four years.

The data suggests that women who work collaboratively with spouses, partners, financial advisors and even knowledgeable friends, report higher confidence in their retirement security. Among men and women, men are more likely, by a margin of 65% to 55%, to calculate retirement income.

"The combination of risks for women and their relatively inadequate retirement planning has become known as the ‘perilous paradox,' but the message is clear that women are able to avoid that," said Sandra Timmermann, director of the MetLife Mature Market Institute. "The risks and costs of ‘living long and living female' call for an ‘affirmative action' plan. We find that those who plan for a steady stream of income, along with some flexibility for the unexpected, are best prepared for what can be an extended future."

Longer life spans for American women create additional costs and financial constraints that can lead to greater financial challenges in retirement, according to the study. As of 2009, women aged 65 years or older had significantly lower annual retirement incomes than men—an average of $21,500 vs. $37,500. American women are more likely to experience retirement alone since many never marry or are widowed or divorced.

If you’re like most people, (both men & women) the thought of developing a comprehensive financial plan that provides you a clear and easy to understand roadmap of your retirement income is easier said than done.

Yet the sooner you know where you stand and how best to move forward, the sooner you’ll enjoy the benefits and peace of mind a solid financial plan brings to your life.

Fair/Not Fair Photo by Xuoan's Dailies

Bogle Discusses Investment Risk During Volatile Times

These are not happy days here in the U.S. With a constant barrage of bad economic news and a stock market that has even the most earnest long-term investor rethinking their investment strategy, hope and optimism is in short supply.

That’s why this week, when the PBS News Hour did a segment on a new book titled: Millennial Momentum: How a New Generation Is Remaking America by Morley Winograd and Michael Hais, I could barely contain my excitement and enthusiasm. Finally, finally, after drowning in a sea of gloomy news comes this inspiring book that can remind all of us intelligent optimists why we prefer to see the glass as half-way full.

Next time you’re stuck at the airport on a business trip or sitting in traffic on the way to or from work, ask yourself this question. If given a choice between a higher quality of life vs. a higher standard of living, which option would I choose?

As we move into a global economy that moves faster and faster and becomes ever more competitive, the question of your money or your life will become ever more relevant. That’s because the financial pressures will continue to increase as will the demands on your time.

Striking a balance between work and play used to be a lot easier. Although this has traditionally been a struggle for most people, now it seems harder than ever. And with a sagging global economy and a roller coaster stock market thrown in the mix, finding time to just clear your head and think about your future is a daunting challenge.

For all the amazing benefits financial planning brings to people lives, perhaps one of the least understood yet most powerful outcomes is giving yourself the freedom and space needed to step back from your day to day routines and check in with yourself.

Although this seems like such an easy exercise to perform, with busy lives and demanding careers, it’s easier said than done. Usually a task like this gets put on that elusive to-do list, never to be seen from again. And before you know it, 10 or 20 years goes by like the blink of an eye. Yet taking the time this year or even next year to stop, slow down and assess where you are and where you’re headed can reap enormous dividends if done well and with unabashed self-honesty.

Ask a small business owner to describe what makes their business tick and most of the time they can answer this question with superb detail and enthusiasm. Now ask this same, passionate, small business owner to describe their overall tax strategy and most likely you’ll hear silence.

Of course this silence is not a mystery. Most small business owners wear at least five hats to begin with when operating their business and their tax and finance hat is usually not one of their favorites. That’s all too understandable, but here’s why it's important to have a tax strategy for your business.

Like any business owner, if you’re profitable, (or even if you’re not) paying taxes is going to be one of your major expenses - many times one of your largest. As a former practicing tax accountant, I wish I could say the tax code is fair and you’re operating on a level playing field. That’s not the case. The deck is stacked against the little guy/gal and until there’s actual and real tax reform, it’s going to stay that way.

Because the tax code is so complicated, most small business owners opt to file a Schedule C - Sole Proprietor return. And because most small business owners in general tend not to be the best record keepers, the IRS loves to audit Schedule C filers. Even if you did everything right and assuming you have nothing to hide, an IRS audit distracts you from your business at hand and very often causes high anxiety and stress.

I’m a big fan of operating your business as an S corporation. It’s not for everyone, that’s for sure. But if you haven’t had a CPA or financial planner run a tax comparison of what business entity would be most optimal to operate your business or practice, I highly suggest you have this analysis done prior to the end of the year.

Very few S corporation tax returns filed each year are audited. In recent years, the audit rate has been 0.40% annually. That’s the kind of odds a tax accountant loves. How does this compare to other business entities audit chances?

• Partnerships: 0.40

• C Corporations: 1%

• Individual’s filing Schedule C: 1.17%

Although statistically there doesn’t appear to be a big difference between an S corporation audit risk and a Schedule C filer - the difference is night and day. With the IRS eagerly on the pursuit for fees and income, becoming a tax savvy small business owner is more important than ever.

data source: TurboTax

photo by saturnism

Although summer is just winding down, it's already time to look at your 4th quarter financial tasks. Here is the last in the four part installment from the Financial Planning Association (FPA) task list.

Last week, one of my investment management clients called and asked me to review his 85 year old mother’s investment statement and offer my opinion about her overall investment strategy or lack thereof. He was worried that his Mom’s portfolio was being churned and burned.

Even before his fax came through, I had a bad feeling. When I reviewed her current investment statement, it didn’t surprise me to see that 85% of her now dwindling portfolio was invested in stocks and that on average, 42 stock trades were being bought and sold each and every month. I wish I could say this was an isolated incident, but it’s not, not by a long shot. Elder abuse, especially when it comes to investing, is on the rise.

I’ve seen enough statements like this one that betray an investor’s trust to last a lifetime. It always gets me thinking - this could be my Mom being taken advantage of.

Who remembers the 7-up ‘un-cola’ commercials? All these decades later I still remember that distinctive voice of actor Geoffrey Holder. If you want a flashback-here he is in a YouTube video that will bring you back in time: 7-up

Talk with any financial advisor about money management, investment strategies, financial planning, you name it, and unless you’ve harbored a secret desire to become a financial advisor yourself, sooner rather than later, your eyes will glaze over and next thing you know you’re thinking about the wood-fired pizza you’re ordering for dinner tonight.

Last week I met with a prospective client that’s an amazingly talented and successful artist with a studio in Bolinas in West Marin County. Lisa (not her real name) is recently widowed after a very long and loving marriage. Her husband was a prominent attorney in San Francisco and handled nearly every aspect of their money management and investments.

If you’re the type of investor that thrives on volatility in the stock market, this is your kind of summer. With the advent of high frequency trading, multiple hedge funds using Wall Street as one big casino, the global sovereign debt crisis, etc, market volatility for at least the short-term is here to stay.

At some point the stock market will bottom out, although when that happens is anyone’s guess. But when that eventual time does come, what happens next is relatively predictable based on past history.

Once the dust does finally settle from this recent market downturn, turn on CNBC or Bloomberg News and watch how the usual suspects describe in elaborate technical fashion why the stock market is now extremely oversold, how the S&P price/earnings ratios are now at historic lows, how there is lots of value in the market at these bargain basement prices and who is buying what at what price.

600 points down in the stock market yesterday, 420 points up today; one can only guess what tomorrow brings our way. If the recent stock market rollercoaster ride has you feeling dazed and confused, you’re not alone.

Transforming your relationship with money is mostly an inside job. Exploring your history, emotions and assumptions around money AND being willing to challenge and change outdated beliefs is easier said than done - yet it must be done.

I don’t know about you, but I’m disgusted with the politics surrounding the increase of the debt limit. This is routine housekeeping work that has turned into hostage taking. Republicans seem to have lost any interest in the belief that we’re all in this together and that we should be looking out for the common good of all and not just the few at the top.

Burn the village to save the village. Let the country default on its debt. The rhetoric being touted by Republicans is dangerous and corrosive to our society as a whole. Those of us in the silent majority that are fed up with this lack of compromise and putting our country first need to let our voices be heard.

If you’re a fan of Dana Carvey and Mike Myers, you know their famous line as Garth and Wayne from Wayne’s World – I’m not worthy, I’m not worthy!

If you have struggled with your relationship with money, you may be having difficulty with the concept of feeling worthy of achieving financial independence and financial success. Here are 7 tips to get you thinking, and acting, like the winner that you are.

If you are like many others, you may think investing is complicated. But by simply knowing your goals and options and then picking the right investing partner, becoming a successful investor is easier than you think. Vanguard does a great job at explaining the steps you’ll need to take in making smart investment decisions as well as guide you on becoming a successful investor. Check out these excellent articles - Vanguard’s 4 Investing Truths:

1) Vanguard’s Investing Truth - RISK:

Trent from The Simple Dollar has written a post called Robinson Crusoe and Our Journey which I had to share with you. This post inspired me to re-read Daniel Defoe’s classic book Robinson Crusoe – so right off the bat, thanks Trent, for the reminder of this not-so-childhood classic.

Trent says the book struck a chord because of his recent journey which appeared to have been about money, but was so much more, in his words, “rethinking what’s actually important to me.” So often this journey is the springboard to discovering what one's relationship with money really is. As a holistic financial planner, I constantly question clients on what it is they absolutely need, what their values are, and as Trent mentions, what is actually important to them.

In my neck of the woods, with the arrival of spring comes the amazing abundance of certified organic farmers markets. In the Bay Area, we are blessed with some of the finest artisan foods a region can offer. As a society we are beginning to understand that the well-being of a region depends on our relationship to our soil and our local food producers. So when it comes to voting with your dollars, one way is to buy your food direct from the farmers that grow it.

Socially Responsible Investing (SRI)

When it comes to investing in Asia, China still gets most of the attention. China continues to attract more investors that any region in Asia, yet, there’s a hidden gem in Asia, namely South Korea, that I believe warrants your attention.

Economic growth remains strong. South Korea’s exports are expected to grow by 11.9%. This is also one of the most wired nations in the world - 95% of homes have broadband, compared with 58% in Germany. South Korea’s economic partnership with China is strong and growing stronger. China now accounts for about 25% of South Korea’s exports.

With the amazing rise in the value of gold, silver and other precious metals in the past few years many investors are looking to cash in on some of the spectacular profits they’re currently sitting on.