As often happens, I learn great lessons about money listening to my clients share their money stories with me. Here’s a story I had to share.

As often happens, I learn great lessons about money listening to my clients share their money stories with me. Here’s a story I had to share.

In an interesting study conducted at the Vanguard Group, they claim that during the financial crisis of 2008 and 2009, among the 2.7 million people with I.R.A.’s at Vanguard, men were much more likely than women to sell their shares at stock market lows.

If there is any truth in this data that says women make better decisions around investing - what is it? Can science provide some answers as to why men lag behind women when it comes to making smart investing decisions?

Could it be the way the male/female brain is built? Is is purely a behavioral difference? What does testosterone have to do with making investment decisions? Does brain imaging technology give us any answers? What might evolution have to do with it?

In this new study by the Vanguard Group, they show some interesting results along with answers that may surprise you. Check out the study in the New York Times article titled How Men's Overconfidence Hurt's Them as Investors.

There’s a new money management website that has a free program called Pocketsmith. On it's web-based calendar, you schedule in your bills, salary, rent, etc. PocketSmith takes the information and generates forecasts which plans your upcoming annual budget. If budgeting and cash flow have been a challenge or you wish there was a calendar program that could help make sure you know when your bills need to be paid, check out Pocketsmith. They also have a decent blog.

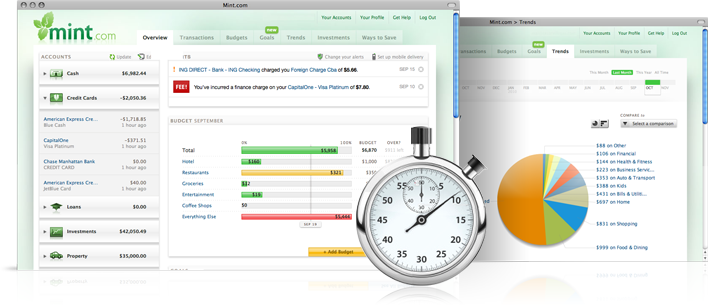

Along with Money Magazine, PC Magazine Editor's and Kiplinger's - I too rate Mint.com as my top choice for a personal financial management tool. Mint's blog is excellent and worth following. The Mint on-line community offers support, Q&A videos and more. Mint.com is a good looking website, easy to follow and simple to use - and it's free. Now there's no reason not to get your personal finances in order.

-How much money do you need to retire, or as I like to say, stop working for money, and not be at risk of outliving your financial resources?

When it comes to managing your personal finances, spending, particularly overspending is one of the most challenging aspects of living within your means. It’s not that you don’t have good intentions, because most people really do want to stay on a spending plan, it’s more complex than that. Spending money causes an emotional rush in our bodies. It’s a natural high. It’s short term pleasure for what could turn out to be long term debt. It’s the nexus between money and your emotional intelligence (EQ) that often creates the problem of overspending.

Create a speed bump on the road to spending

For many investors, low cost index funds are just too boring. Here’s an article from the New York Times by Paul Sullivan titled, Index Funds, Dowdy to Some, Get Notable Endorsement, that adds some gravitas to the fans of index funds.

He interviews Burton Malkiel, author of investment advice books,who practices what he preaches. In his retirement portfolio, he says "all the serious money is indexed."

Latest post from The Economist: New Dangers for the World Economy - not for the faint of heart, but definitely worth a read.

Visiting clients at their home is old school, I know that, but I still love it. Sometimes I feel like the small town doctor making house visits. At a recent client meeting in Sebastopol, CA, before we moved into the discussion about financial planning, my clients shared pictures of baby grey foxes that set up home right in their front yard.

Another local client always wraps up our meetings by opening a bottle of his own estate grown wine. Living in wine country feels like a movie set as we sip and chat while overlooking his beautiful vineyards.

From the start of the financial crisis right up until today, we have been bombarded with story after story of how much wealth was vaporized from the global financial system. It seems all the news is about dollars and cents. How much did your 401k or 403b go down? How about your IRA’s, your home value? Everything is focused on the material-money, and little conversation is had discussing the emotional, physical and spiritual ramifications this crisis is having on regular people’s lives.

As a financial planner working mainly with couples, I see firsthand the damage this crisis has had and continues to have on relationships. Let’s face it; money is a tricky enough subject to deal with when things are good. But when the s**t hits the fan, whether it’s a job loss, too much credit card debt, too much spending, not enough saving, you name it, the inability to communicate and resolve conflict grows and grows and the risk to your relationship grows as well.

For the most part, financial planning and money in general is pretty serious and heavy stuff to deal with. So when there’s an opportunity to take a break and laugh, why not, right? Check out this YouTube video, Financial Planning 101:

{kind=link}